Introduction

Singapore has earned its place as one of the world’s most trusted destinations for business and investment. With a stable political climate, transparent regulations, and a pro-business environment, it continues to attract entrepreneurs and global companies seeking a gateway to Asia. Its strong legal system, advanced infrastructure, and ease of doing business make it a preferred choice for international expansion.

Foreign investors are particularly drawn to Singapore for its favourable tax framework, wide network of trade agreements, and efficient company incorporation process. The city-state’s focus on governance, innovation, and global connectivity reinforces its reputation as a secure and dynamic base for growth.

Under Singapore law, anyone conducting business activities for profit on an ongoing basis must register an entity with the Accounting and Corporate Regulatory Authority (ACRA). This ensures compliance with statutory obligations and gives businesses the legal standing to operate within the country.

This guide explains how foreigners start a business in Singapore and outlines the process to register a company in Singapore for foreigners, from choosing the right business structure to meeting local residency requirements and filing through BizFile+. With the right preparation and professional guidance, establishing a business in Singapore can be a smooth and rewarding process.

Key Takeaways:

- Foreign investors can establish and fully own a Singapore company, provided they meet local residency and representation requirements set by ACRA.

- Selecting the right entity type, such as a private limited company or branch office, determines liability, compliance scope, and long-term scalability.

- Partnering with a qualified corporate service provider helps streamline incorporation, ensure accurate filings, and maintain governance standards.

- Singapore’s transparent regulations, favourable tax framework, and strategic location continue to attract global entrepreneurs seeking a stable base for regional growth.

Establishing a Business Presence in Singapore

Setting up a business in Singapore is a clear and structured process designed to support transparency and investor confidence. To register a company in Singapore as a foreigner, it is important to understand how ownership rules, residency conditions, and statutory requirements set by ACRA work together to ensure compliance.

Singapore allows full foreign ownership while requiring local representation to meet regulatory obligations. With proper planning and professional support, foreign entrepreneurs can establish a credible and compliant business presence built for long-term success in the region.

The Business Landscape for Foreign-Owned Companies

Singapore provides one of the most open and supportive environments for international investors. Foreigners are allowed to own 100% of a Singapore-registered business entity, giving them full authority over corporate decisions, shareholding structures, and management operations. This flexibility enables entrepreneurs to operate independently without local shareholder involvement.

However, each company must appoint at least one locally resident individual in a key management or representative role. This ensures there is an authorised point of contact within Singapore for regulatory communication and compliance purposes. A locally resident person may be a Singapore Citizen, Permanent Resident, or a valid Employment Pass or EntrePass holder.

Foreign Identification Number (FIN) holders should confirm their eligibility with the relevant authority, such as the Ministry of Manpower (MOM) or the Immigration and Checkpoints Authority (ICA), before accepting an appointment. This step ensures compliance with ACRA’s statutory requirements for company officers.

Many foreign investors choose Singapore as their regional base due to its extensive trade agreements, robust legal protections, and strong financial infrastructure. The country’s transparent legal system, efficient dispute resolution mechanisms, and reliable banking network further enhance its reputation as a trusted destination for Singapore business registration for overseas investors.

For entrepreneurs planning long-term expansion across Asia, understanding the foreign business setup requirements is an essential first step before proceeding to register a company in Singapore as a foreigner.

Choosing the Right Type of Business Entity

The type of entity you choose when you register a company in Singapore as a foreigner will determine your business’s legal liability, compliance obligations, and eligibility for government schemes or tax incentives. As long as residency and statutory requirements are met, foreigners may incorporate any of the following entities through ACRA.

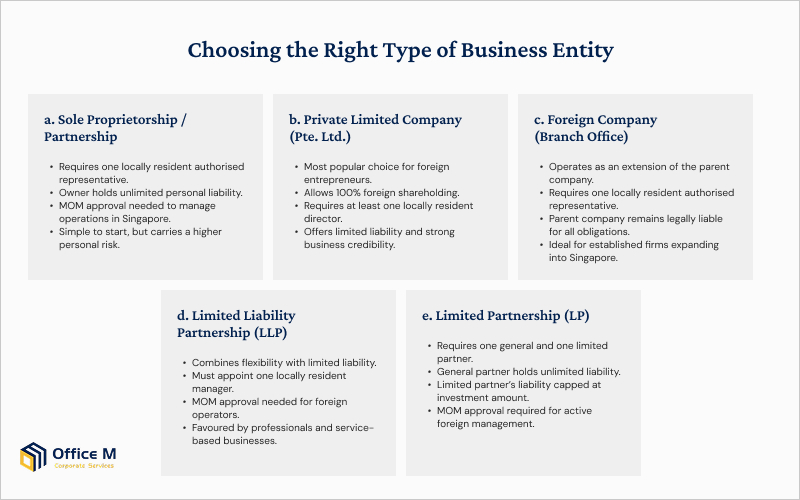

A. Sole Proprietorship or Partnership

Foreigners may set up a sole proprietorship or partnership in Singapore, but at least one locally resident authorised representative must be appointed. This individual assumes full personal liability for the business and acts as the main point of contact for regulatory purposes.

Foreign entrepreneurs residing overseas who wish to manage their business directly in Singapore must first obtain approval from the Ministry of Manpower (MOM). Although this structure is straightforward and affordable, it carries higher personal risk because liability is not separated from the owner. For this reason, it is less commonly chosen by those looking to register a company in Singapore as a foreigner.

B. Local Company (Private Limited Company)

The Private Limited Company remains the most preferred structure for investors planning to register a company in Singapore as foreigners. It allows 100% foreign shareholding and requires at least one locally resident director to meet ACRA’s statutory requirement.

This model offers limited liability protection, ensuring that shareholders’ personal assets are not affected by company debts or obligations. It also enhances business credibility when dealing with clients, financial institutions, and investors. For entrepreneurs seeking scalability, stability, and compliance assurance, the private limited company structure offers the most suitable foundation for growth.

C. Foreign Company (Branch Office)

An overseas corporation can register a company in Singapore as a foreigner by establishing a branch office. This option allows the foreign company to extend its operations to Singapore while remaining legally part of its parent entity. At least one locally resident authorised representative must be appointed to oversee compliance.

While a branch office can carry out the same business activities as its parent company, it does not enjoy separate legal status. This means the parent company remains liable for all obligations incurred in Singapore. Branch offices are typically chosen by established businesses expanding into the market without forming a new incorporated entity.

D. Limited Liability Partnership (LLP)

An LLP combines the flexibility of a partnership with the protection of limited liability. It must appoint at least one locally resident manager who is responsible for ensuring compliance with Singapore’s laws and annual filing requirements.

Foreign entrepreneurs based overseas must designate a local manager, while those intending to operate within Singapore need MOM approval before commencing operations. Many consultants, designers, and professional service providers opt for this structure when they register a company in Singapore as foreigners because it allows shared management while limiting personal exposure to risk.

E. Limited Partnership (LP)

A Limited Partnership consists of at least one general partner and one limited partner. The general partner must be locally resident and holds unlimited liability, whereas the limited partner’s liability is confined to their investment amount.

Foreigners wishing to actively manage an LP within Singapore must obtain approval from MOM before taking up the role. As with other structures, the appointed local partner or manager bears responsibility for ensuring that the partnership complies with ACRA’s regulations.

Each entity type presents unique advantages based on your business goals, level of control, and appetite for risk. For investors assessing how foreigners start a business in Singapore, understanding these structures ensures a well-informed decision before proceeding to register their company.

Incorporation and Application Process

The process to register a company in Singapore as a foreigner is completed through BizFile+, the Accounting and Corporate Regulatory Authority’s (ACRA) online filing portal. While the overall procedure is straightforward, the exact steps may vary depending on the applicant’s residency status, visa type, and eligibility to access the system.

For Foreigners with an EntrePass

Foreign entrepreneurs holding an EntrePass can apply directly through BizFile+ using their SingPass credentials. During the application, they must submit:

- A proposed company name for ACRA’s approval.

- Details of all shareholders, directors, and company officers.

- The company constitution and supporting identification documents.

Once the application is approved, ACRA issues a Unique Entity Number (UEN) to confirm successful incorporation. This streamlined process allows EntrePass holders to manage their registration independently without engaging local intermediaries.

For Foreigners without an EntrePass

Foreigners who do not hold an EntrePass must engage a corporate advisory firm in Singapore, such as a law firm, accounting practice, or professional corporate secretarial agency, to file the application on their behalf. These authorised agents assist with name reservation, document preparation, and the submission of incorporation details in compliance with ACRA regulations.

This arrangement is necessary to register a company in Singapore as a foreigner, as BizFile+ access is restricted to users with valid SingPass credentials, which non-residents typically do not possess.

Supporting Steps Before and After Incorporation

- Company name approval: The proposed company name must be approved by ACRA before incorporation. It should be unique, appropriate, and free from conflicts with existing registered entities or trademarks.

- Document preparation: Key documents include the company constitution, Know Your Customer (KYC) verifications for all shareholders and directors, and signed consent-to-act forms. These ensure transparency and compliance with regulatory standards.

- Appointment of a local representative: At least one locally resident director or authorised representative must be appointed before the company can be registered. This individual acts as the official point of contact for statutory matters.

- Online filing: Incorporation details are submitted via BizFile+, ACRA’s online system. Most applications are processed within one to three working days, provided all documentation is in order.

- Opening a corporate bank account: After incorporation, a corporate bank account should be opened with a licensed financial institution in Singapore. Some banks may require directors or signatories to be present for identity verification and due diligence checks.

Additional Administrative Considerations

Professional firms providing company incorporation services often offer ongoing administrative and compliance support to help businesses stay organised after registration. These services may include:

- Appointment of a qualified company secretary to meet statutory requirements.

- Maintenance of statutory registers, meeting minutes, and corporate records.

- Preparation and filing of annual returns and other documents with ACRA.

Foreign applicants should engage an experienced agent familiar with BizFile company registration for foreigners to ensure that all documents are correctly prepared and filed. Fees typically vary depending on the complexity of the application and any additional services required, such as appointing a nominee director or arranging an office address rental in Singapore for official correspondence.

Partnering with a trusted corporate advisory firm allows entrepreneurs to register a company in Singapore as a foreigner while meeting all foreign business setup requirements and maintaining a credible, compliant business presence.

Compliance and Ongoing Obligations

Once you register a company in Singapore as a foreigner, your responsibilities extend beyond incorporation. Every Singapore-registered company must meet ongoing statutory requirements, such as appointing key officers, maintaining accurate records, and submitting annual returns and tax filings on time.

Understanding and fulfilling these obligations helps foreign business owners maintain compliance, demonstrate sound governance, and uphold credibility with ACRA, IRAS, and other regulatory authorities.

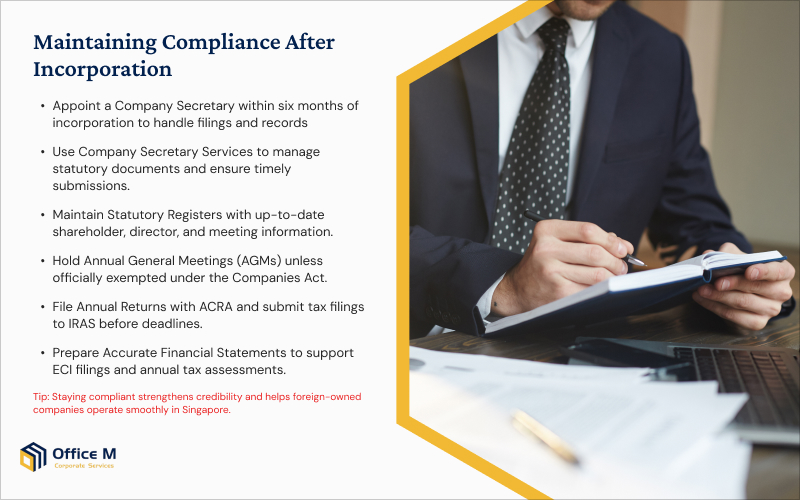

Maintaining Compliance After Incorporation

After you register a company in Singapore as a foreigner, ongoing compliance is vital to keeping your business in good legal standing and avoiding penalties. All companies must meet statutory obligations outlined by the Accounting and Corporate Regulatory Authority (ACRA) and the Inland Revenue Authority of Singapore (IRAS). These include:

- Appointment of a company secretary within six months of incorporation. Many foreign entrepreneurs engage professional company secretary services to ensure proper record-keeping and timely submissions.

- Maintenance of statutory registers and company records, covering shareholder, director, and meeting information.

- Holding of Annual General Meetings (AGMs) unless exempted under the Companies Act.

- Submission of annual returns to ACRA and corporate tax filings to IRAS within the prescribed deadlines.

- Preparation of accurate financial statements to support Estimated Chargeable Income (ECI) submissions and tax assessments.

Adhering to these requirements demonstrates strong corporate governance and enhances trust with regulators, financial institutions, and business partners. Engaging a professional corporate advisory firm helps ensure all documentation and filings are managed efficiently, allowing you to focus on business growth with confidence.

Relocation, Passes, and Local Management

Foreign entrepreneurs who wish to relocate to Singapore and manage their operations directly can apply for an Employment Pass or EntrePass, depending on their business model and investment scale. The EntrePass may be submitted either before incorporation or within six months after registration. Each application is reviewed by the Ministry of Manpower (MOM) based on business viability, applicant experience, and potential contribution to Singapore’s economy. This flexibility makes it easier for foreigners to establish and register a company in Singapore with long-term operational control.

For those already residing in Singapore, Dependants’ Pass holders may apply for a Letter of Consent (LOC) to run a business after incorporation with ACRA. Individuals holding a Foreign Identification Number (FIN) should confirm eligibility with MOM before accepting roles such as director, secretary, or manager.

Entrepreneurs who prefer to manage their company from abroad can continue doing so, provided at least one locally resident director or authorised representative remains appointed to ensure compliance. Many business owners engage professional firms that offer nominee director services to fulfil this statutory requirement reliably and transparently. This arrangement allows foreigners to register a company in Singapore while maintaining proper local representation and regulatory accountability.

Questions You Might Have

Is 100% foreign ownership allowed?

Yes. Foreigners can own 100% of a Singapore-incorporated business without the need for local shareholders. This gives full control over business decisions, profit distribution, and shareholding structure. However, to register a company in Singapore as a foreigner, at least one locally resident director or authorised representative must still be appointed to satisfy ACRA’s statutory requirements.

Do I need to be in Singapore to incorporate a company?

No. You do not need to be physically present in the country to register a company in Singapore as a foreigner. The entire incorporation process can be completed remotely through a registered agent or corporate advisory firm. Most steps, including company name reservation and constitution submission, are carried out online via ACRA’s BizFile+ system. However, some banks may require directors or authorised signatories to attend an in-person verification meeting before opening a corporate bank account.

What is the minimum capital required?

The minimum paid-up capital for incorporation in Singapore is S$1, which makes it accessible for startups and small enterprises. There are no restrictions on the currency used or when capital can be increased. Many businesses raise their paid-up capital after incorporation to enhance credibility, meet visa eligibility criteria, or qualify for specific licences and government grants.

Can a dependant’s pass holder run a business?

Yes. Dependants’ Pass holders may operate a registered business after obtaining a Letter of Consent (LOC) from the Ministry of Manpower (MOM). The LOC allows them to take part in daily operations or management of their company. Those who prefer not to relocate can continue managing operations remotely, provided a locally resident manager or director is appointed to oversee compliance matters.

What support is available for foreigners after incorporation?

Foreign entrepreneurs can access professional assistance from corporate service firms that handle ongoing compliance and administrative responsibilities. These specialists manage statutory filings, maintain company records, and ensure timely submissions to local authorities. Engaging such support allows business owners to maintain compliance and focus on growth, making it easier to register a company in Singapore as a foreigner and operate sustainably in the long term.

Conclusion

The process to register a company in Singapore for foreigners is straightforward and supported by a business environment built on transparency, efficiency, and trust. While the incorporation framework is designed to be accessible, understanding local residency requirements, company structure options, and ongoing compliance duties is essential to operating confidently and legally.

Foreigners can fully own a Singapore-registered company but must appoint at least one locally resident director, manager, or authorised representative, depending on the entity type. All applications are filed through ACRA’s BizFile+ platform. For those without an EntrePass, engaging an experienced corporate advisory firm ensures that every step of the process is completed accurately and in compliance with statutory timelines.

With its stable governance, pro-business tax system, and strategic connectivity, Singapore remains a leading choice for entrepreneurs worldwide seeking to register a company in Singapore as foreigners and build a long-term presence in Asia.

Office M supports foreign business owners through every stage of incorporation, offering structured guidance in compliance, nominee directorship, and corporate governance. Contact Office M today to begin your incorporation journey with confidence and establish a trusted foundation for your business in Singapore.

officem

officem